Global Pension Underfunding Will Hit Nearly Half A Quadrillion Dollars In 2050

ZeroHedge.com

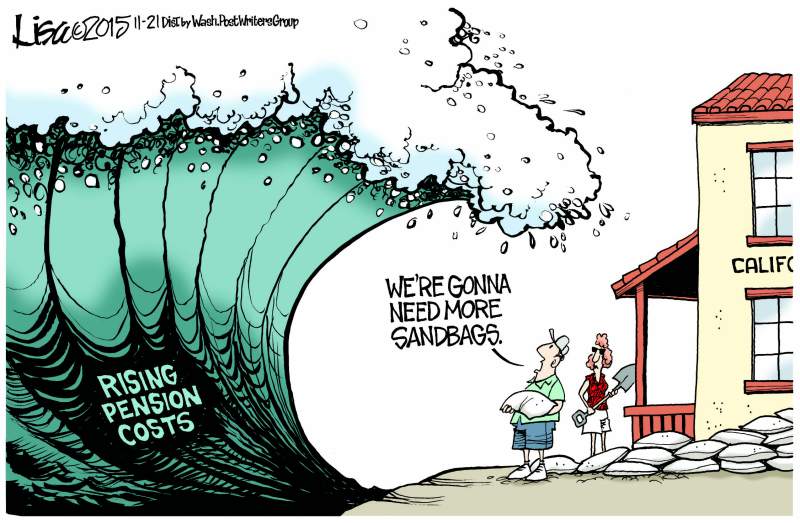

Earlier this week we highlighted “Six Terrifying Graphs That Summarize America’s Public Pension Crisis” which ranked state, county and city-level public pensions in the United States by which are screwed the most. To summarize, the study concluded that public pensions in the U.S. alone are currently underfunded by nearly $4 trillion and that taxpayers in Illinois, California and New Jersey should probably be looking to move before getting drowned in their state’s coming pension-induced tax hike tsunami.

Of course, as we’ve argued before, the current pension underfunding levels are sure to only get worse over the coming decades as the world will have to contend with a wave of retiring Baby Boomers and a period of lackluster, volatile returns. So how bad could the global funding gap get? Unfortunately, the World Economic Forum (WEF) recently set out to solve that impossible math equation and it turns out the answer is about $400 trillion…give or take a couple trillion.

Not surprisingly, the WEF attributed their terrifying conclusion to an ageing population, lack of savings, low expected growth rates and financially illiterate citizens.

Long-term, low-growth environment: Over the past 10 years, long-term investment returns have been significantly lower than historic averages. Equities have performed 3%-5% below historic averages and bond returns have typically been 1%-3% lower. Low rates have grown future liabilities, and at the same time investment returns have been lower than expected and unable to make up the growing pension shortfall.

Inadequate savings rates: To support a reasonable level of income in retirement, 10%-15% of an average annual salary needs to be saved. Today, individual savings rates in most countries are far lower. This is already presenting challenges where traditionally defined benefit structures would have provided a guaranteed pension benefit. Now, as workers look at their defined contribution retirement balances, with no guaranteed benefits, they are realizing that the retirement income their savings will provide will be much lower than expected.

Low levels of financial literacy: Levels of financial literacy are very low worldwide. This represents a threat to pension systems which are more selfdirected and which rely more on private savings in addition to employer- or government-provided savings.

Of course, ignoring that minor ~20 year increase in life expectancy over the past 60 years without raising retirement ages can take a toll on those present value calculations of future liabilities.

Oh, and turns out that politicians creating massive ponzi schemes to promise citizens that their government would take care of their financial needs in perpetuity, while never really bothering to explain the true costs of such programs, was probably a bad idea.

But luckily these politicians are exempt from being prosecuted for their financial crimes…so taxpayers will just have to deal with picking up the $400 trillion tab.

The full WEF study can be viewed here: