The Great Wave off Kanagawa (神奈川沖浪裏) Source: public domain

JAPAN: An Economy On Life Support And The Looming Financial Disaster

TMR Editor’s Note:

The following intelligence briefing prepared by Jim Autio at DEEP CONNECTIONS on the true state of Japan’s economy and its financial status is both shocking yet unsurprising. It has been common knowledge to those in the investment banking industry that Japan’s economy has been on “life support” for many years now. What Jim has done is accurately illustrate just how serious the situation really is.

Because this intelligence briefing is a living document, the reader is advised to consult the following link where they will be privy to the latest updates. Japan’s economic condition and financial health change by the day, and DEEP CONNECTIONS stays on top of those changes. The repercussions of not doing so are too great for those who invest in both Tokyo real estate and Japanese financial investments.

JAPAN Gray Swan: http://medium.com/deepconnections/prevailing-gray-swans-3-august-19-2016-b907b50ab921#.z5i5j42kf

For high integrity information concerning other major gray swans flying around the globe, please click on the links below:

The Millennium Report

August 31, 2016

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Prevailing Gray Swans: The Clear and Present Danger List for the Week Ending August 26, 2016

Submitted by James Autio

Intelligence Analyst

3. Economic collapse of Japan

Deep Background and Threat Forensics: Briefing Focus

[economics | finance | politics | sociology]

Understanding the sheer gravity of the perilous position of Japan is not difficult provided you cut through the surface fog and focus on the deep structural issues. What frames the analysis are: the oldest population on earth, the highest public debt-to-GDP by a large margin, and a flat GDP. Japan has been a background gray swan for many years because of these factors; what upgrades the collapse of Japan from a background gray swan to a prevailing gray swan is that multiple structural factors have hockey stick-shaped curves and the escalating numbers have reached unprecedented levels that have now qualitatively shifted from the upper limits of rational thought to crossing the River Isis* over to the other side — to the irrational, even to the phantasmagorical.

Think of an infinite force pushing against an immovable object — something must give, but what, how, and when? That is where Japan, and by intimate association — we — are now.

A Calculus of Hockey Sticks

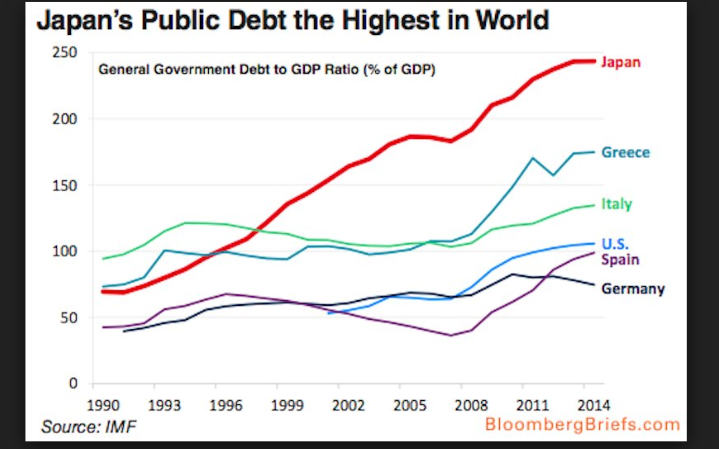

- Debt-to-GDP

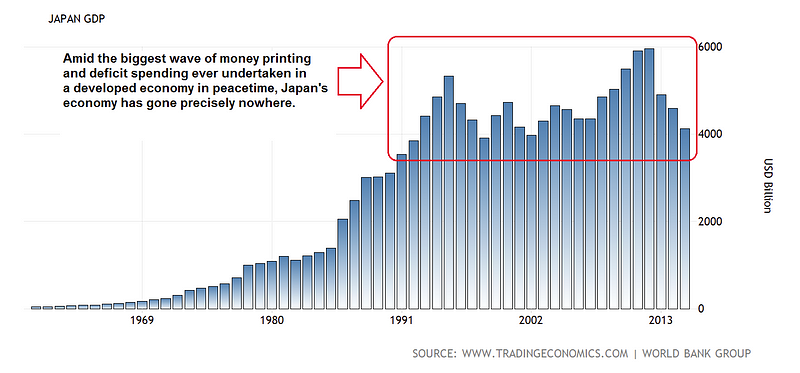

GDP has been in decline…

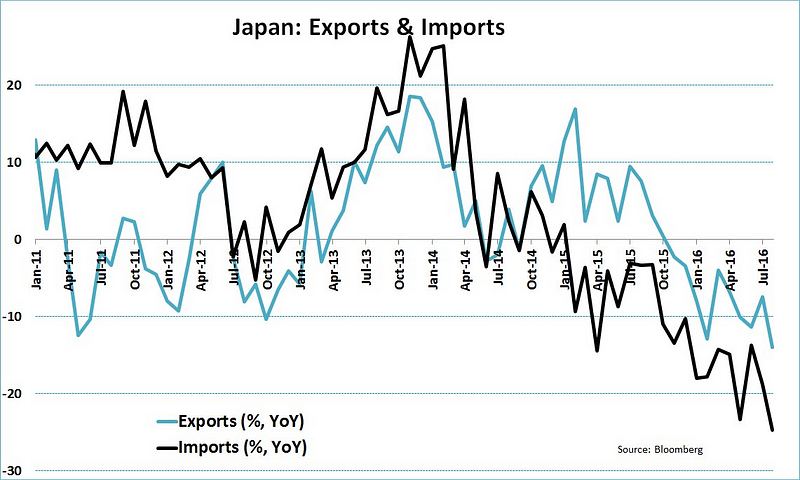

with exports in decline since October 2015…

…but Debt-to-GDP is steadfast with its upward climb.

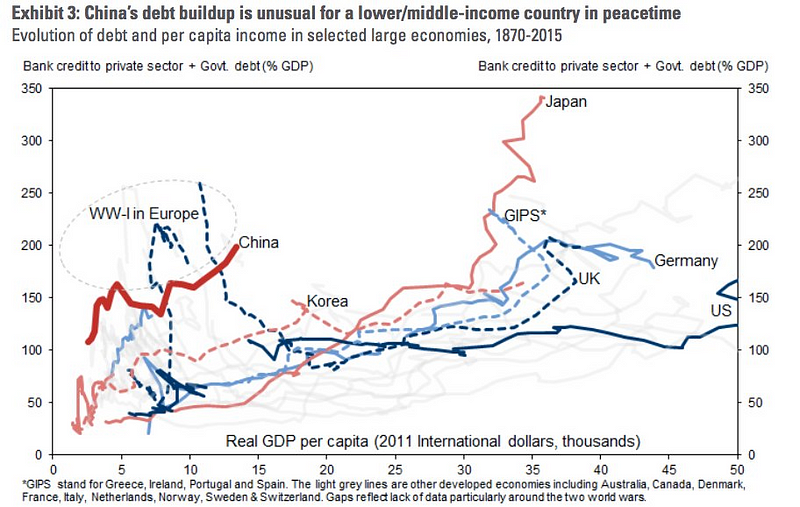

Japan has a level of debt to GDP that is profoundly greatly than any other developed country including Greece:

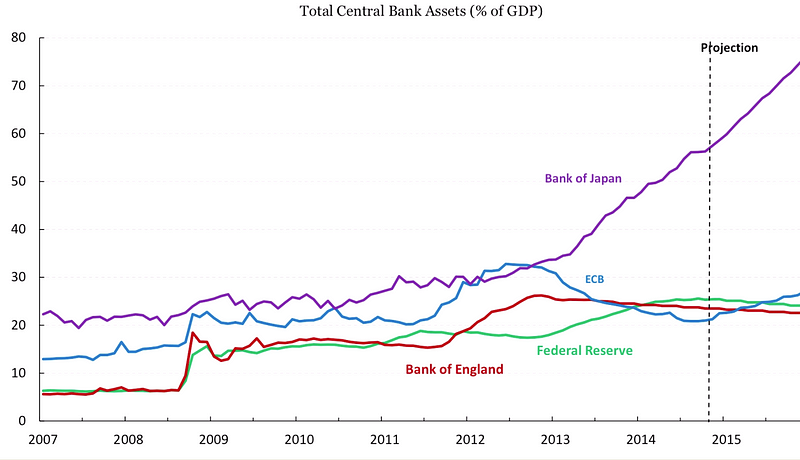

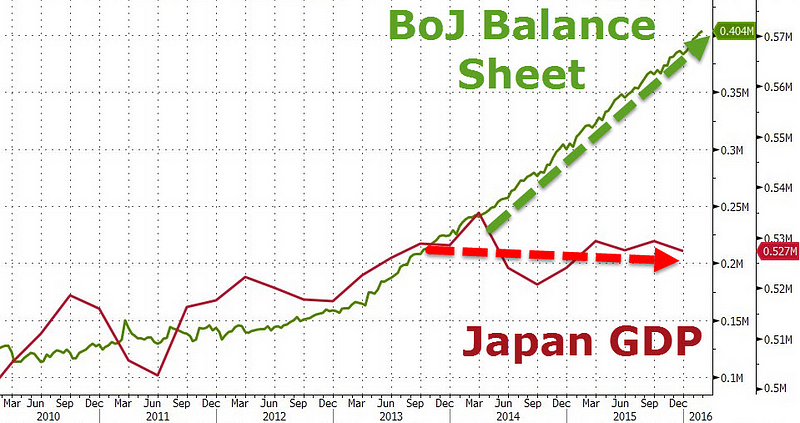

2. The central bank of Japan (BOJ) has a balance sheet that is going vertical

Compared to other central banks:

Stark divergence of BOJ balance sheet from GDP:

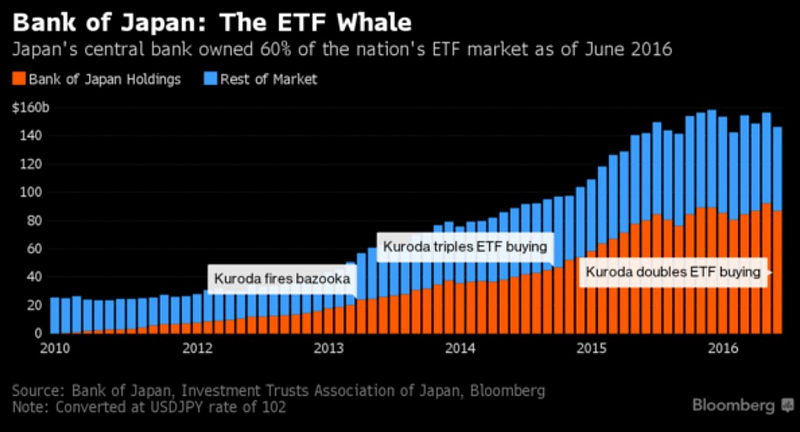

Hockey stick increase in central bank purchase of Japan’s equity market via ETF purchases:

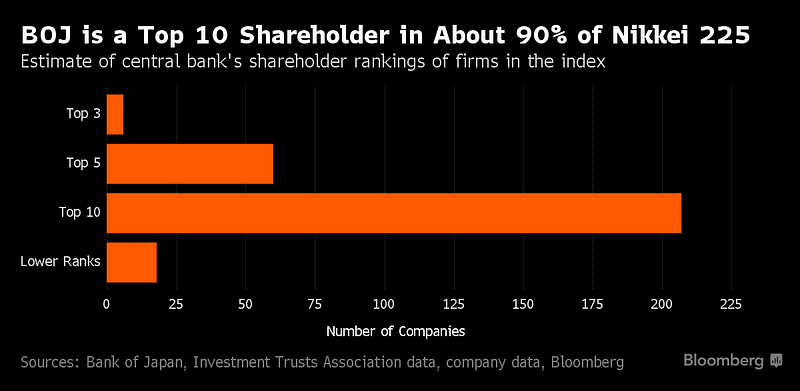

BOJ has morphed into a hedge fund colossus that has become the world’s largest purchaser of Japanese stocks on the Nikkei 225:

While the Bank of Japan’s name is nowhere to be found in regulatory filings on major stock investors, the monetary authority’s exchange-traded fund purchases have made it a top 10 shareholder in about 90 percent of the Nikkei 225 Stock Average, according to estimates compiled by Bloomberg from public data. It’s now a major owner of more Japanese blue-chips than both BlackRock Inc., the world’s largest money manager, and Vanguard Group, which oversees more than $3 trillion.

(Source: Bloomberg, April 24, 2016, “The Tokyo Whale Is Quietly Buying Up Huge Stakes in Japan Inc.”)

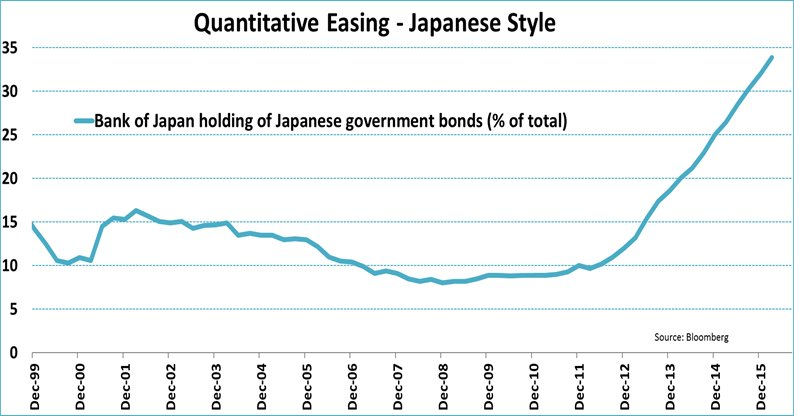

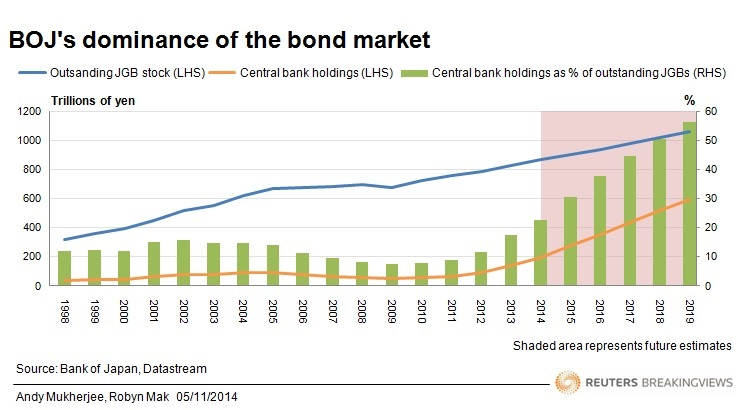

In parallel, BOJ has become the largest purchaser of Japanese sovereign bonds (JGB):

And the purchase of JGB is going vertical on a multi-year event horizon to the point of becoming the lion’s share of all JGB issuance:

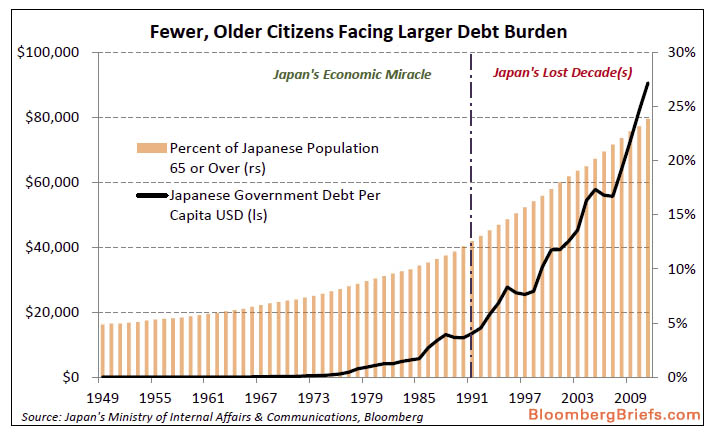

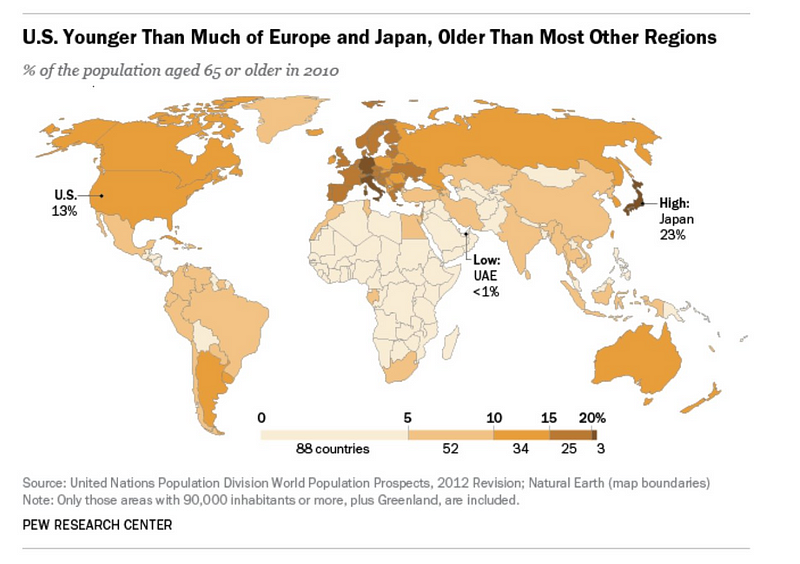

3. Japan’s retirement population is the largest in the world and is going vertical

Japan’s debt per capita is going vertical at the same time that the retirement cohort is going vertical:

The debt per capita is going vertical which will be inherited by the Productive-Age Population and eventually by the Child Population with nothing to show for it meaning that Japan’s monetary strategy automatically creates a massive “negative inheritance” for future generations. Since the population is shrinking while the debt is going vertical the result is an exponentially accelerating debt per capita that is crippling.

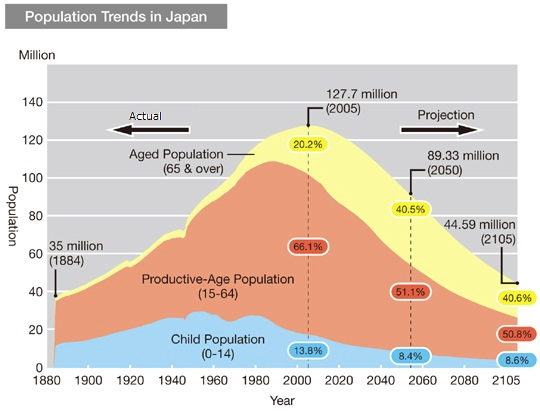

Japan’s population over the age of 65 compared to other countries:

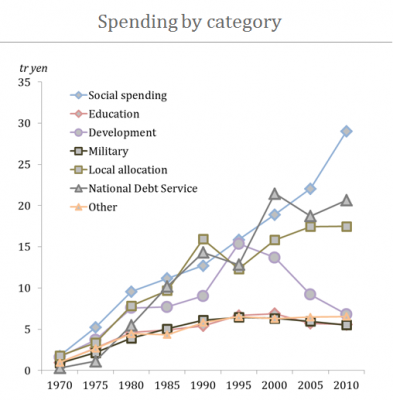

4. Social spending is going vertical in proportion to the growing retirement-age population (this is causal not merely correlative)

For Japan is not only in a dire fiscal situation, they are also the oldest country in the world. Social spending is growing exponentially and the demographic dividend they enjoyed up to the mid-1990s is now turning against them. There will be many more dependents and far fewer breadwinners as we move forward. The demographics in Japan would overwhelm the country even if their fiscal situation was sound.

(Source of quote and chart: Eugen von Böhm-Bawerk, July 28, 2013, “Japan; from quagmire to Abenomics to collapse! Part II”)

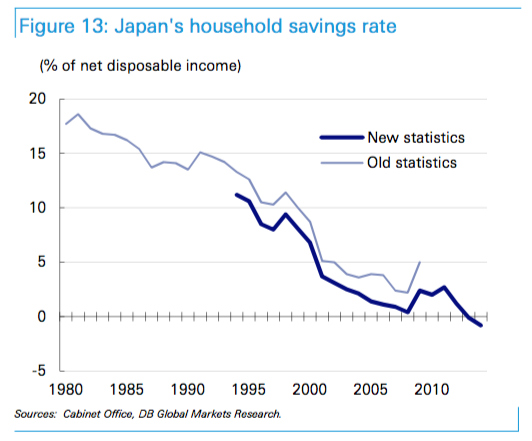

The Japanese population has shifted from net savers to dissavers (i.e. “spenders”) as the retiree-to-worker ratio has crossed a threshold which is backed by a structural tailwind; this constitutes an important new trend with important consequences:

Public debt is reaching ridiculous levels and spending will only grow from here. When big bulges of old people start to retire they will be dissaving and it will be impossible for the big banks to use excess deposits to roll over government debt. Collapse is at this stage inevitable.

(Source: Eugen von Böhm-Bawerk, July 28, 2013, “Japan; from quagmire to Abenomics to collapse! Part II”)

Japan Is Structurally Constrained: An Infinite Force Pushing Against an Immovable Object

Japan now has a mathematical predicament that cannot be ignored any longer, it has hit a wall: social costs are rising due to aging demographics; GDP is flat and taxes cannot be materially increased; the extraordinary public debt has interest payments that eat the budget to the point they mustplateau or decrease; and military spending needs to increase due to Chinese territorial exploits but is strapped.

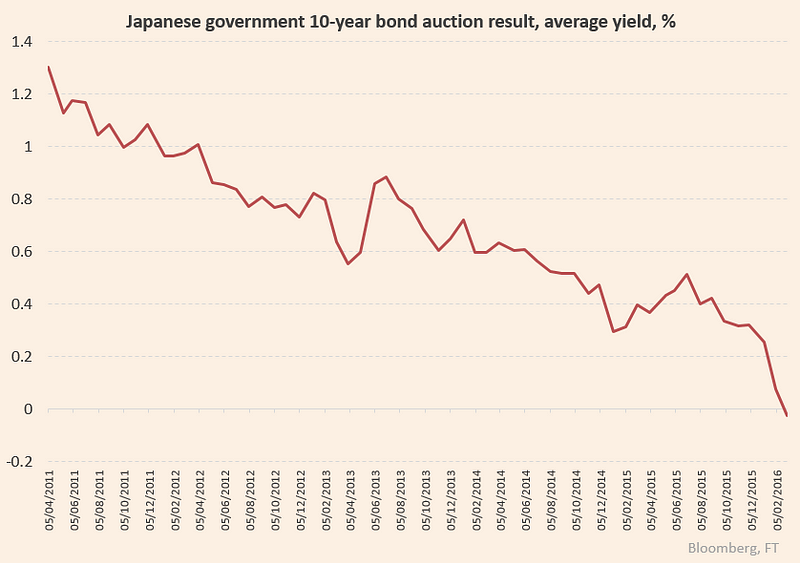

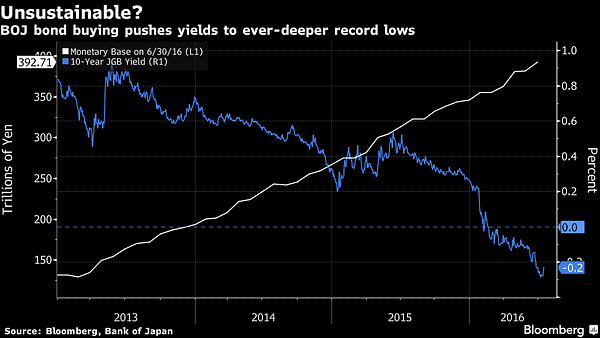

Remedy: In 2012 Kuroda steered the 10 year GJB to under a 1% yield and has been on a mostly linear decline to close to the zero-bound (ZIRP or zero interest rate policy) reached in 2016:

Despite this move, interest payments continued to rise because of the scale of their purchase during a non-stop QE program beginning in 2012 (“Abenomics”):

More specifically we know spending on interest is increasing even though the BoJ manipulates JGB rates lower. Think about that for a second. Even as interest rates paid falls, total spending on interest rises. Now, assume the price inflation rate goes to two percent annual rate. Holding a 10-year JGB at 80 basis points does not make any sense as the bond holder will lose 120 basis points per year. It is not crazy to assume the 10-year at 3.5–4.0 per cent if the BoJ succeed. For a country that has to refinance almost 200 trillion yen per year plus a deficit of 50 trillion, basis points counts. If we add 200 basis points to the average interest paid on outstanding loans, interest payments would soar from 10 trillion to 25 trillion! Interest payment alone would then constitute 27 per cent of total outlays or 70 per cent of tax revenues!

(Source: Eugen von Böhm-Bawerk, July 28, 2013, “Japan; from quagmire to Abenomics to collapse! Part III”)

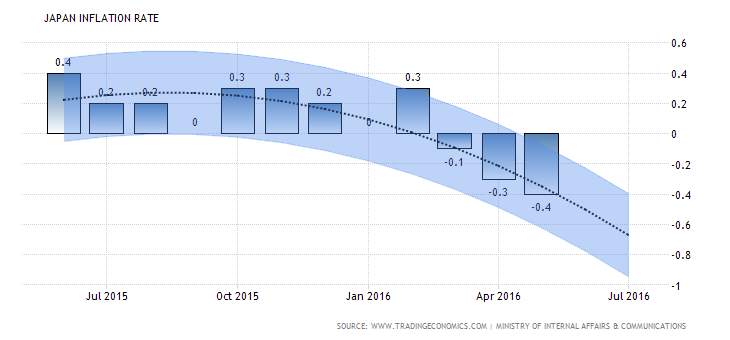

Yes, theoretically, QE and “Abenomics” should have increased the inflation rate which is a stealth means to dilute the debt if controlled (i.e. the debt is paid back to creditors with a less valuable currency, a stealth form of currency debasement that flies under the radar). But inflation has failed to materialize:

ZIRP has failed to increase GDP and has failed to increase inflation (mild deflation instead). So, what next?

Introducing NIRP (negative interest rate policy)

This is the part of the story where we must ford the River Isis*. The consequences of NIRP — on a global scale — is a Prevailing Gray Swan all to its own.

Kuroda and the BOJ’s policy makers voted 5–4 to approve NIRP and the measure was adopted on February 16, 2016 [Video: see Kuroda’s public announcement of NIRP]. NIRP, like ZIRP, has failed to provide the projected benefits and has largely backfired with the exception of effects on debt servicing costs (given the extreme government debt load, net interest ratesmust be extremely low and are trapped there which constrains monetary policy flexibility).

One of the theoretical benefits of NIRP was to be strongly bullish on the NIKKEI 225 but, instead, has been flat to mildly bearish — in any case, no fireworks to the upside:

Consequences of ZIRP and NIRP So Far in Japan

Japan has the appearance of being bulletproof through decades of facing converging, hockey-stick structural problems. But cracks are beginning to show and where there’s smoke there’s fire. When NIRP is sustained and treated as policy instead of a transient, fat-finger blip, what happens? What are the unintended consequences? Are they directly derivative of NIRP per seor are they Japan-specific? Japan is the G-7 Judas goat and some of the EU have followed suit.

Stress on JGB primary dealers

NIRP has seriously impacted the JGB primary dealers and the biggest one is opting-out as a market maker:

The top executive of Japan’s biggest bank delivered a rare criticism of the central bank, saying its negative interest-rate policy has contributed to anxiety among households and companies and prolonging it may weaken financial institutions.

“Both households and businesses have become skeptical about the effectiveness of policy measures to address the current economic problems,” Nobuyuki Hirano, president of Mitsubishi UFJ Financial Group Inc., said Thursday in a speech in Tokyo. Declines in banks’ net interest margins “will become even more severe and protracted by the implementation of the negative interest-rate policy,” he said.

Hirano said there’s “no guarantee” that negative rates will encourage companies to increase capital spending because low borrowing costs and deflation have been “business as usual for over a decade.” Lenders won’t be able to pass on negative rates to individual and corporate depositors, he said in English at a conference of international bankers. Politicians and analysts have also criticizedthe negative-rate program, which has reduced interbank lending, prompted money-market funds to stop accepting cash, and failed to stem gains in the yen.

(Source: Bloomberg, April 13, 2016, “MUFG Chief Criticizes BOJ’s Policy for Fueling Japan Anxiety”)

“Bank of Tokyo-Mitsubishi UFJ has informed Japan’s Finance Ministry that it will cease to serve as a market maker for Japanese government bonds, a move driven by the growing burden of holding the notes under negative interest rates.”

(Source: Nikkei Asian Review, June 14, 2016, “BTMU says it will drop out as JGB primary dealer”)

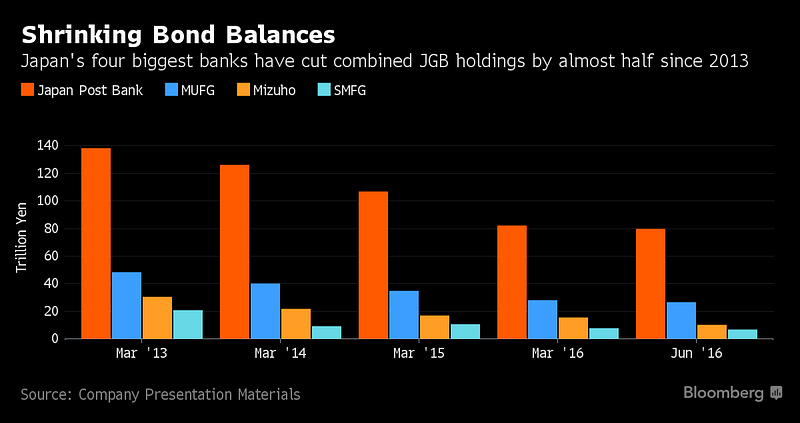

It is the largest reduction in JGB holdings among the three megabanks, and the group now holds the smallest amount of government bonds among the three. Having started to unload government debt before the other megabanks did, the group is not in a particular hurry to give up its primary dealer status.

Despite their reduced portfolios, the megabanks still hold a combined 54 trillion yen in JGBs. If they further unload government bonds, prices could fall and interest rates could rise. The BOJ and commercial banks have supported massive issuances of government debt. But commercial banks, which are accountable to shareholders, operate under different circumstances from the central bank.

(Source: Nikkei Asian Review, June 16, 2016, “Japan’s megabanks step away from JGBs”)

The people are angry

Japan as a society has been asleep through decades of money printing but now they are awake: NIRP has served as a Japanese alarm clock to the rank-and-file, not just astute banking CEOs like Nobuyuki Hirano:

The Bank of Japan’s surprise move into negative interest rate territory has been associated with a series of unintended consequences that complicate the country’s growth and financial stability outlook. From more illiquid markets for government bonds to indications that households are disengaging from the financial system, along with greater political scrutiny of the central bank and swelling popular anger about its policies, there is growing awareness of potential collateral damage.

(Source: Bloomberg, Mohamed El-Erian, April 13, 2016, “Cracks in system: Japan people disengaging from the system, people angry”)

Premonitions of capital flight that could seal the fate of Japan’s future

Simply: sustained NIRP + ZIRP has created a ghost town in new JGB purchases with the last buyer standing being the BOJ. What is in the wind is a migration from JGBs to US Treasuries because of the attractive yields at equivalent tenor (i.e. same time period). This trend, once it reaches critical mass, will drive UST yields down while JGB yields rise from the sell-off. This is a means for rationale albeit incredibly patient and patriotic Japanese (and other international, diversified investors) to reluctantly throw in the towel and vote with their feet.

(Source: Bloomberg, August 1, 2016, “Treasury 30-Year Yield Seen Near Zero in Nomura’s Vicious Circle”)

Long-term slow growth in the world’s largest pension fund with recent big losses

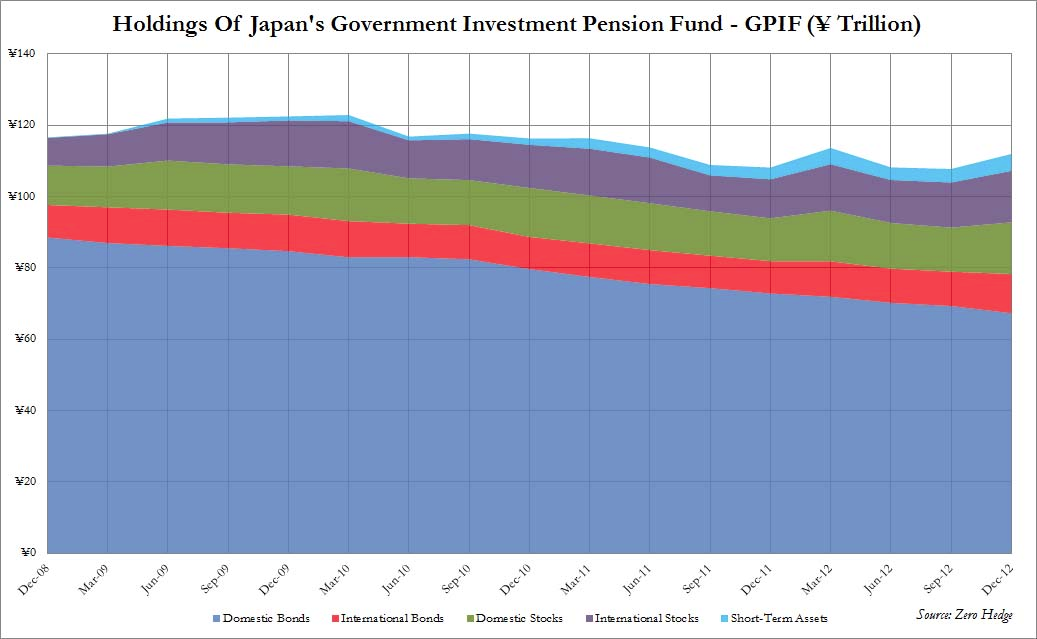

During the ZIRP to NIRP policy experiment there have been huge losses in the world’s biggest pension fund, Japan’s Government Pension Investment Fund (GPIF)…

From March 31, 2009 to June 30, 2016 (the last 6 fiscal calendar years plus the quarter from April 1 to June 30, 2016) GPIF’s holding increased from ¥118T to ¥129.7T which is only a 9.9% net increase in 6 years and 3 months.The last quarter from April 1 to June 30, 2016 suffered a loss of ¥5.2T (3.9%)followed by a ¥5.0T loss during the previous fiscal year. (The ZIRP to NIRP transition occurred in mid-February for the JGB 10Y bond). Pension funds typically need a 7% CAGR (compound annual growth rate) to be viable. In the world’s oldest society, this does not bode well.

But there is a great irony here: GPIF sold JPG bonds recently at significant profit because of the bull market for bonds — when yields go down prices go up. It was the NIKKEI that suffered recently; the losses in GPIF occurred in stocks, not bonds. But with bonds now at sky-high prices due to NIRP, what will the GPIF do next?

Time to rebalance the portfolio with stocks. But, in the big picture, the NIKKEI will have two whale buyers putting a floor under the Japanese stock market: the BOJ and the GPIF. There are two takeaway messages: (1) hedge funds et al are going to front-run (i.e. buyers are going to rush in before the slower moving whales make their purchases to maximize their profits at BOJ’s, GPIF’s, and pensioners’ expense) and; (2) corporate earning don’t matter when you have whale buyers making indiscriminate stock purchases through index ETFs that include all the large market cap companies on the NIKKEI exchange.

Battered Tokyo stock investors may find savior in an old friend: the world’s biggest pension fund.

Because shares held by Japan’s $1.4 trillion Government Pension Investment Fund have suffered such large losses, it will need to add to those holdings to meet targets for their weighting, while selling sovereign bonds whose value has soared. Morgan Stanley MUFG Securities Co. estimates that, assuming no re-weighting was done since Jan. 1, GPIF will need to buy 4.2 trillion yen ($42 billion) of local stocks and sell 9.8 trillion yen of Japanese government bonds to reach its goals. The brokerage didn’t give a time frame for this buying.

(Source: Bloomberg, July 7, 2016, “Stock Losses Force World’s Biggest Pension Fund Into More Buying”)

Japan’s Final Act: Crossing the River Isis to the Wonderland of Helicopter Money

“I trust that many of you are familiar with the story of Peter Pan, in which it says, ‘the moment you doubt whether you can fly, you cease forever to be able to do it,’” Bank of Japan Gov. Haruhiko Kuroda said at a conference hosted by the BOJ.

“For central bankers, the challenges over the past two decades have been daunting, as they navigated economic booms and busts, relying on previously untested monetary means to keep the global economy on an even keel”, he said.

“Each time central banks have been confronted with a wide range of problems, they have overcome the problems by conceiving new solutions,” Kuroda said. “I am sure that we all can share a conviction backed by our collective experience and wisdom.”

(Source: Japan Times, June 5, 2015, “The Peter Pan approach to central banking — Kuroda wants to fly”)

There is clear evidence that current monetary policy is effective. Inflation and growth are improving moderately.

— Haruhiko Kuroda (@HaruKuroda_BOJ) May 6, 2016

ZIRP failed. NIRP is failing. If insanity is doing more of the same and expecting different results then that sound logic should kill-off taking bond yields to subterranean minus-1 or beyond. The idea was to stimulate the economy by offering ultra-low interest loans to corporations (practically free money) to encourage them to spend on capex (capital expenditures) and to nudge investors, pension funds, and insurance companies into equities to underwrite growth or at least give the illusion of growth. ZIRP and NIRP are theoretical tools to stimulate economic growth. But when released into Japan’s ecosystem it failed and more of the same is clearly not the answer. The money never materialized as consumption; the Japanese GDP has remained moribund while the structural hockey sticks go straight-up. The C-suites of Japanese corporations are smart; consumer demand is not there — you cannot push on a string no matter how hard you push.

Japan was the G-7 Judas goat for ZIRP, NIRP, and pushing the sensibility envelope of debt-to-GDP. The EU and US observed the sky didn’t fall; the limit has not been discovered — yet. But it is not safe to assume Japan, the EU, and US have the same tolerances to these stresses and that it is a cakewalk to these extraordinary levels of debt so close to crush depth. Assuming Japan is a trial balloon for grandiose monetary and fiscal experiments is a big mistake. Japan is socially an insular society and has nearly a zero-tolerance immigration policy. The evolutionary outcome over most of recorded history is a powerful cohesiveness derived from Japan’s homogeneity and belief systems — their collective view results in an unselfish “we” as opposed to a selfish “me.” The Japanese people will not abandon ship, they will go down solemnly together as an integral society. Their collective perception and values are not shared by the two Americas or Europe. Even China has evolved toward the West in this regard (e.g. look at capital flight).

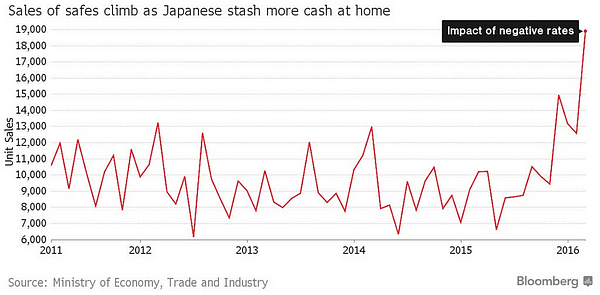

However, despite Japan’s incredible cohesiveness, cracks are showing. It will be a fracturing of this social cohesiveness that will pop the many historic, gargantuan bubbles that have defied the sharpest pins for so long. NIRP was the dawn of the forthcoming collapse with its division-by-zero aura, Japan is now wide awake to financial follies that result in such startling singularities of logic. In response, the Japanese people have created a hockey stick of their own to counter the thieving effects of negative rates:the purchase of safes to harbor physical cash and monetary metals. The Japanese people have been cynical of Prime Minister Shinzō Abe and theLDP leadership but it has truly been a frustrating case of: “Abe is the worst Prime Minister we have ever experienced…except for all the others.” Even though he is re-elected, there is a stark lack of political capital to robustly back a mandate; the problem at hand is that there is a growing loss of trust in the very leaders that hold the keys to the people of Japan’s future and this has now emerged as a tip-of-the-spear Achilles’ heel — and more will follow suit. Anger — albeit subdued, which is the Japanese way of expressing discontent — is present in the social subconscious and that is an anxious and doubtful genie you can’t put back in the bottle. It will take deeds, not dialogue, or a Hail Mary.

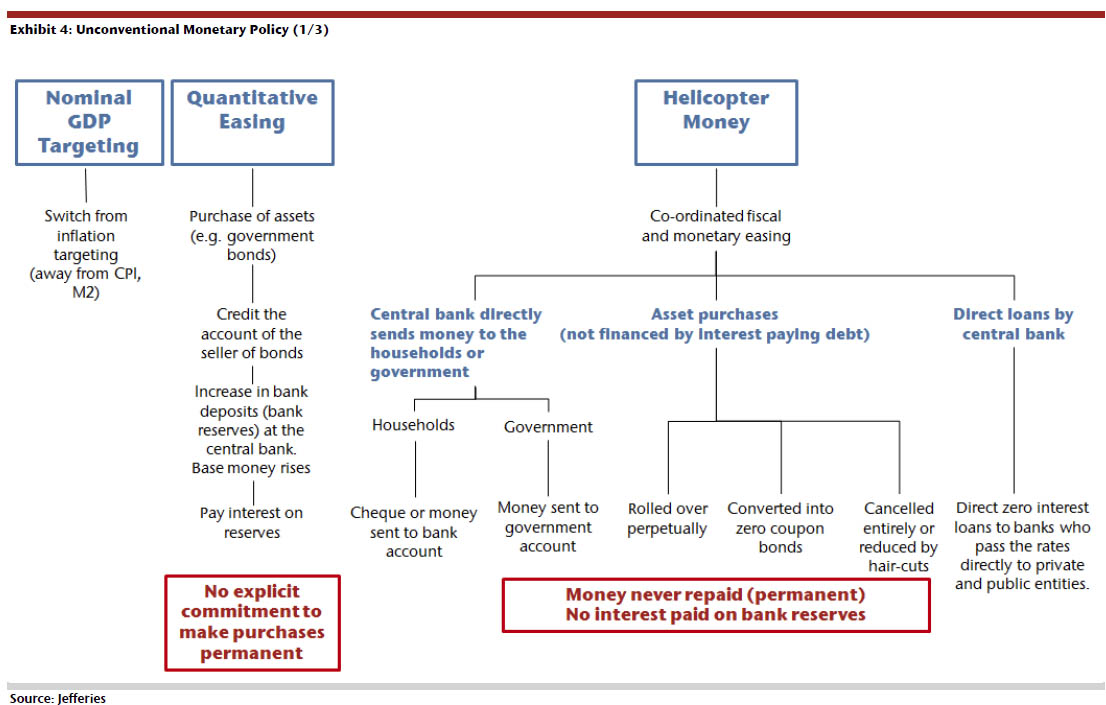

Paying someone to borrow your money stretches the minds of even the most imaginative souls but helicopter money one-ups that. In theory it shouldn’t, but in practice it does. With NIRP you can’t just go to a bank and ask for money and in return they will mail you a check every month. But in some helicopter money schemes, they do send you a check or there are some hoops to jump through to get it. As an aside, Japan is already doing a quasi-form of helicopter money: BOJ purchasing vast amounts of equity ETFs does qualify as “free money” to shareholders and, unlike Quantitative Easing (QE), shareholders are not limited to banks — any shareholder can sell those shares and pocket the money that fell from the sky. It’s just that the common people are not beneficiaries of this largess, only the top 15% and the lion’s share is concentrated in the top 0.1% like high-networth individuals, hedge funds and sovereign wealth funds. But it is a big step toward free money for all.

The problem with quantitative economic models like QE and other exotic unconventional monetary policies is that they fail to account for the consequences of tears in the social fabric caused by loss of trust — it is hubris to believe that inflation can be contained once Pandora’s box is opened.

Here are some of the schemes that Japan may entertain:

Jefferies’ Global Head of Equity Strategy Sean Darby believes that the ultimate end game would be a conversion of the BoJ’s negative-rate bond holdings into perpetual zero coupon bonds. This would effectively turn the bonds into worthless pieces of paper. And it would ease the government’s debt-to-GDP ratio and clear the way for tax cuts and spending hikes.

(Source: The Fiscal Times, July 12, 2016, “Can ‘Helicopter Ben Bernanke’ Save Japan?”)

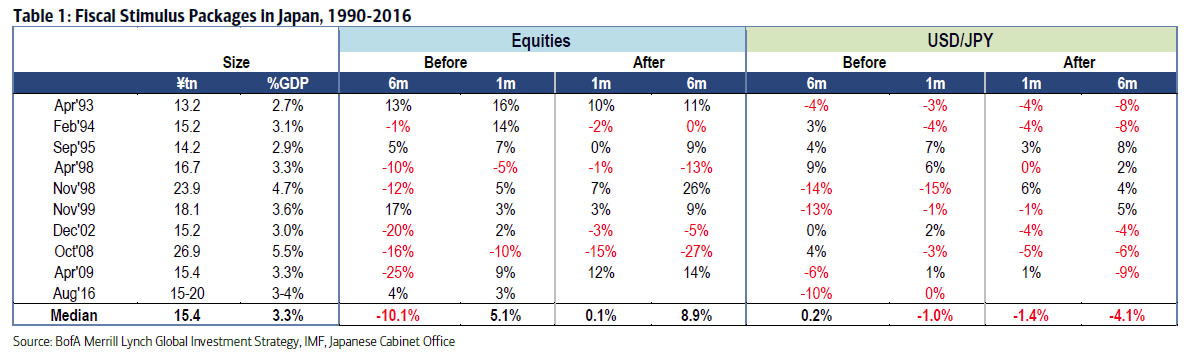

Japan has nearly a 25 year history of large “stimulus” packages and Michael Hartnett, Chief Investment Strategist at B of A Merrill Lynch just published what the effects have been on the yen and NIKKEI stock market:

Big Japan fiscal stimulus = +ve Nikkei: Table 1 shows dates, size of 10 largest Japan fiscal stimulus packages since 1990; average size = 3.4% of GDP; fiscal stimulus often enacted after stocks down big prior 6 months; stocks rally 1 month ahead of fiscal announcement, pause in weeks after package announced, then rally in subsequent months; meanwhile Japanese yen tends to strengthen after the policy announcement; a >¥15–20tn Japan fiscal stimulus announcement in coming weeks financed with implicit BoJ helicopter money would help keep risk rally alive until Labor Day.

(Source: BofAML (Michael Hartnett), July 22, 2016, via ZeroHedge)

[Second opinion on an upcoming stimulus based on a helicopter money scheme: July 11, 2016, Nordea Bank AB]

What is predicted in the near future (August) is a ¥15–20T fiscal stimulus in some form of helicopter money. In the table, pay particular attention to the ineffectiveness of these large stimulus packages. Another one will balloon the hockey stick bubbles closer to thin air.

Will Japan move forward with a helicopter scheme? At this point it is the next play in the playbook. There has been much recent talk about it even with reference to Depression Era Japan when in late 1931 Korekiyo Takahashi was installed as the new finance minister and implemented monetary policy that successfully resulted in reversing a stifling deflationary economy which included currency devaluation as a remedy. Will such an approach work again? 2016 is not 1931. Besides the unorthodoxy of helicopter money on the economic and financial levels it has enormous influence on psychological, sociological, and technical levels which, for the most part, are ignored but bear enormous impact on cause and final effect in our complex, interconnected world.

Understanding the real-world consequences of very high-stakes economic theory such as NIRP and helicopter money lies at the turbulent intersection of state-of-the-art network theory and primeval sociology — reflexivity(not limited to George Soros) and animal spirits will move markets somewhere, all while brewing in a fluid and quixotic ecosystem of high-frequency trading volume, multiple species of nascent, predatory AI algorithms parsing the waters, front-running insiders at TBTF banks, and mega-volume hedge-fund carry trade operators. Now add to this dynamic brew the BOJ juicing the system while, perhaps, doing currency swaps with the US Fed. Most of these entities are selfish actors interacting in a multi-player, nonzero-sum game theory framework but at the systems-level there will be collective behaviors that operate with positive (amplification, 1 + 1 = 3) or negative (suppression, 1 + 1 = 0) synergies…it all depends on the conditions which change at fractal time scales: millisecond, minute, hour, day, and month with each having its own niche all while nested within each other like an Amazonian swamp spanning bacteria to crocodiles to thunderclouds. Every blip on a chart is the net outcome of all this activity — why do you believe you understand it? Do you honestly think any human is capable of predicting which way is up, let alone managing it once you set it free in the digital wild? Herding cats comes to mind immediately. The current global financial ecosystem, from a network perspective, is not even remotely comparable to previous eras, toy textbook assumptions, or static quantitative models. Advice: To navigate this swamp you need to know as many assumptions as you can. The roots of human nature, crowd behavior, and state-of-the-art AI are a terrific start.

Ramifications

What snake oil is to a quack, helicopter money is to a central banker. Both are proposed cures for real ills, but both are impotent. And fraudulent.Caveat emptor. Understand: A fiat currency has only one of two fates: default or hyperinflation. Helicopter money is a harebrained theory that posits that a blindfolded high-wire walker traversing the Grand Canyon can waltz forever without falling to the left or right. Betting on a fall is a sure thing.

Helicopter money is an egregious affront to a fiat currency’s reputation — money is more than pixel dust on a computer screen. A fiat currency’s strength is directly proportional to each bearer’s confidence and trust of those in charge — after all, it is just a piece of paper; it is what the paper symbolizes that matters and it is the Herculean task of government “to do whatever it takes” to make the common people believe in the integrity of that symbol for as long as possible before it vanishes into the thin air from which it arose.

Helicopter money tests the resolve of any human’s beliefs in the nature of work ethic and productive effort as both a personal and social contract whilst forcefully trivializing any viable concept of store of value or utility. It’s simply a reach too far into the twilight zone. Integrity — somewhere in the stream of commerce’s food chain — is compromised and everyone becomes aware of this social injustice sooner or later. Thus, one day, when loss of trust goes viral, chaos and barter follow like night follows day. Paper with ink becomes no different than paper without it.

Prudent Actions to Strongly Consider

Some form of helicopter money will land on the shores of Japan sooner or later because it is the only endgame remaining. It will be called something else, probably in some arcane academic lingo, but once you deep-dive to the bottom of the rabbit hole please don’t be surprised by the mammoth printing press behind the curtain.

There are no specific actions you can take.

How are these intelligence briefings created?

Prepared by: James Autio

doctorgo@gmail.com

NOTES

*When central bankers must quote Peter Pan to clarify radical intensions, that sends a clear signal that we have ventured away from the realm of logic, rationality, and prudence and into the Wonderland of Lewis Carroll.

Isis, of course, is also the name of the branch of the Thames River upon which Lewis Carroll took the real-life Alice and her sisters on that fateful boating expedition. As just as Isis descends into the Egyptian underworld by way of a boat on the River Nile, so in the prelude poem Alice and her sisters descend into Wonderland by way of a boat on the River Isis.

In the Egyptian underworld, called the Duat, everything is a reverse of the living world. This matches Alice’s anticipation as she falls down her rabbit-hole: she thinks she may end up in the “Antipathies” (instead of the antipodes). She is not entirely wrong, for everything and everybody is contrary to her expectations.

— Quote from Alice’s Adventures in Wonderland Decoded by David Day

___

Prevailing Gray Swans (3): August 26, 2016 – DeepConnections – Medium