Canada’s Housing Bubble Explodes As Its Biggest Mortgage Lender Crashes Most In History

ZeroHedge.com

Call it Canada’s “New Century” moment.

We first introduced readers to the company we said was the “tip of the iceberg in Canada’s magnificent housing bubble” nearly two years ago, in July 2015 when we exposed a major problem that we predicted would haunt Home Capital Group, Canada’s largest non-bank mortgage lender: liar loans in particular, and a generally overzealous lending business model with little regard for fundamentals. In the interim period, many other voices – most prominently noted short-seller Marc Cohodes – would constantly remind traders and investors about the threat posed by HCG.

Today, all those warnings came true, when the stock of Home Capital Group cratered by over 60%, its biggest drop on record, after the company disclosed that it struck an emergency liquidity arrangement for a C$2 billion ($1.5 billion) credit line to counter evaporating deposits at terms that will leave the alternative mortgage lender unable to meet financial targets, and worse, may leave it insolvent in very short notice.

As part of this inevitable outcome, one which presages the company’s eventual disintegration and likely liquidation, Bloomberg reports that the non-binding rescue loan with an unnamed counterparty will be secured by a portfolio of mortgage loans originated by Home Trust, the Toronto-based firm said in a statement Wednesday. Home Capital shares dropped by 61% in Toronto to the lowest since 2003, dragging down other home lenders. Equitable Group Inc. fell 17 percent, Street Capital Group Inc. fell 13 percent, while First National Financial Corp. declined 7.6 percent. In short, the Canadian mortgage bubble has finally burst.

Some more details on HCG’s emergency source of funding: Home Capital will pay 10% interest on outstanding balances and a non-refundable commitment fee of C$100 million, while standby fee on undrawn funds is 2.5%. The initial draw must be C$1 billion. The loan has an effective – and very much distressed – interest rate of 22.5% on the first C$1 billion, declining to 15% if fully utilized, according to a note from Jaeme Gloyn, an analyst at National Bank of Canada.

Home Capital said the credit line is intended to “mitigate” a sharp drop in Home Trust’s high-interest savings account balances, which sank by $591 million from March 28 to April 24, at which point the total balance was $1.4 billion. Home Capital warned on Wednesday that further outflows are anticipated.

Translated: what until last night was a depositor bank jog just became a sprint.

The loan will provide Home Capital with more than C$3.5 billion in total funding, more than twice the C$1.5 billion in liquid assets it held as at April 24. It also has C$200 million in securities available for sale, and high interest savings account balances fell about 25% to C$1.4 billion over the past month. Home Capital relies on deposits to fund their mortgage loans; following today’s announcement the company’s liquidity is certain to get even worse as all non-distressed sources of cash are pulled.

Cited by Bloomberg, Andrew Torres, founding partner and chief investment officer at Toronto-based Lawrence Park Asset Management said that “The company is facing a bit of a liquidity crunch and they felt they needed to resolve it quickly.” He said the “steep” commitment fee and the interest rate on the loan “are surprising numbers for a company that was ostensibly investment-grade.”

Well, it was only investment grade because as usual the rating agencies never did their homework. For a real hint into the company’s rating, look at the 22.5% interest rate, suggesting the company’s days outside of bankruptcy are numbered.

Home Capital Group’s sudden collapse was actually visible from a distance. While in the summer of 2015, the termination of HCG was still debate, in recent months the company’s woes stemmed from allegations by the Ontario Securities Commission that Home Capital misled investors and broke securities laws.

In other words engaged in those “liar loans” which we first warned about back in the summer of 2015.

Meanwhile, founder Gerald Soloway will step down from the board when a replacement is named and Robert Blowes will assume the role of interim chief financial officer, the company said Monday.

“The company anticipates that further declines will occur, and that the credit line would also mitigate the impact of those,” Home Capital said.

Amusingly, it was just two months ago when the company set new performance goals after reporting quarterly results, targeting revenue growth of 5% or greater, diluted earnings-per-share of 7% or greater and a return on equity of 15 percent or more over the long term, according to Bloomberg. It should add one more “performance goal” – stay out of bankruptcy for at least 3 months.

“They did what appears to be to us a very expensive deal,” said David Baskin, president and founder of Baskin Wealth Management in Toronto, a former investor in Home Capital stock. “Basically they blew up the income statement in order to save the balance sheet, which I guess if you’re facing an existential crisis is what you have to do.”

The Office of the Superintendent of Financial Institutions (OSFI) told Canada’s BNN it does not comment on specific institutions it supervises, but that it maintains ongoing relationships with those institutions and is monitoring the Home Capital situation “closely.”

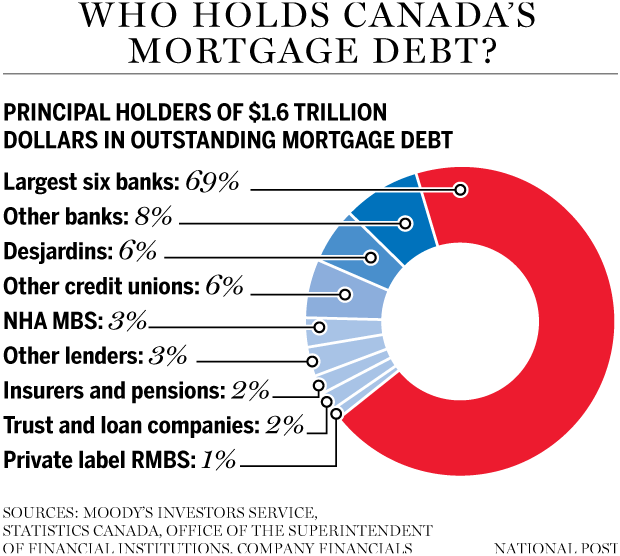

Canada’s entire mortgage lending market is tumbling.